Recent headlines have highlighted the failure of SVB Financial Group, the parent company of Silicon Valley Bank (“SVB”). To help both current and future clients, using publicly available financial records of SVB, including the last two annual reports and every 10-Ks and 10-Q filed this decade, a team of Perficient team members from around the world have gone beyond the headlines to analyze what the root cause of the run on the bank was, and what our clients and us can both learn from the mistakes made at SVB.

As Warren Buffet once said, “It’s good to learn from your own mistakes. It’s better to learn from other people’s mistakes.” We’re putting this into practice and offering our predictions concerning what regulations may arise once the dust has settled.

Possible Causes of Failure

1. Short Capital?

SVB Financial had Tier 1 risk-based capital of 15.40% as of December 31, 2022, over 80% higher than the 8.50% regulatory required ratio. Including reserves, the parent company had Total risk-based capital of 16.18%, more than 50% higher than the required ratio of 10.50% for large banks.

Don’t like or trust risk-based ratios? The Tier 1 leverage capital ratio of the firm was 8.11%, more than twice the 4.00% required by regulators.

| December 31, 2022 | SVB Financial | Bank | Required Ratio |

| CET1 risk-based capital | 12.05% | 15.26% | 7.00% |

| Tier 1 risk-based capital | 15.40 | 15.26 | 8.50 |

| Total risk-based capital | 16.18 | 16.05 | 10.50 |

| Tier 1 leverage | 8.11 | 7.96 | 4.00 |

Perhaps capital was not the primary cause of the bank’s failure.

2. Overpaid Executives

We’re not going to name names, but certain Senators from the great state of Massachusetts came out and declared that the failure was from “weaker regulation,” “lax regulatory supervision,” and “lower capital requirements,” as well as “millions in bonuses” paid by the bank.

While certain members of Congress seem to have made up their minds, let’s see if the facts get in the way:

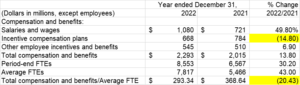

As shown above, the total compensation and benefits cost per employee fell by more than 20% in 2022.

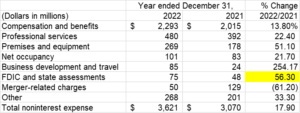

But the fault is the regulators’, right? Shown below is the 56% increase in FDIC and state bank regulator assessment charges. Note the 56% increase in 2022.

Perhaps the cause of the collapse was something other than excessive compensation costs and disinterest from regulators.

3. Loan Issues – Too many loans? Did loan margins decline when rates rose in 2022?

At times in the past, some banks have had difficulties due to loans accounting for too high of a percentage of total assets. Loans are less liquid than many other interest-earning assets, so regulators encourage bank executives to ensure loans are not excessive. In addition to the volume of loans, the margin of loans must be monitored to ensure that as rates change in the marketplace, the interest margin on the bank’s loan portfolio will adjust in lockstep.

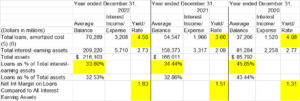

A review of the volume of SVB’s loan portfolio as a percent of total average assets and total interest-earning assets shown above and the net interest margin of the loan portfolio compared to the earnings on Total interest-earning assets reflect that the loan portfolio was contributing positively to SVB’s asset quality and earnings.

4. Securities

4a. Poor Quality?

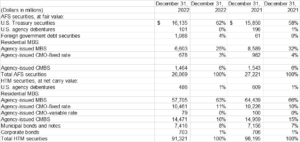

Let’s take a look at the quality of the SVB Financial portfolio, both in the Available for Sale (AFS) and the Hold to Maturity (HTM) segments of the overall investment portfolio:

Lots of US Treasury, mortgage-backed securities, and Collateralized Mortgage Obligations. One veteran Perficient analyst mentioned it looked similar to the savings and loan crisis (S&L) and savings bank portfolios they used to see in the late 1980s and early 1990s.

From a default perspective, the portfolio looks of very high quality.

4b. Interest-Sensitive Long-Term Bonds?

Fixed-rate debt is more price sensitive to changing interest rates than variable-rate debt. Higher-yielding bonds are less sensitive to rising rates than lower-coupon bonds. Long-term debt is more price sensitive than shorter-term debt. Putting that together, long-term fixed-rate low-yield debt is the most sensitive to price changes when interest rates rise.

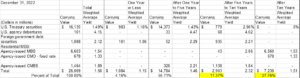

Looking at the year-end AFS portfolio above, almost 40% of the AFS bond portfolio was in fixed-rate, low-yielding bonds with a maturity of more than five years, and more than 25% was longer than 10 years.

The rising interest rate environment in 2022 resulted in the $26 billion of bonds available for sale worth $2.5 less than book value, meaning the firm would have to recognize significant losses should the bonds have to be sold to meet deposit withdrawals, as shown below:

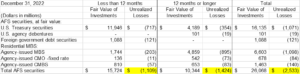

Turning to the largest component of the SVB balance sheet, the Hold to Maturity bond portfolio, we see the following distribution of debt by quality and maturity as of year-end 2022:

Note that almost 95% of the HTM bond portfolio was in fixed-rate (only 0.74% was variable rate), long-term (more than 10 years to maturity), and low-yield (1.63%) debt. In the rising interest rate environment, management had invested like an S&L executive of the 1980s and had a similar outcome.

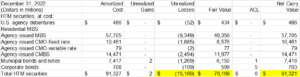

SVB had over $91 billion of high-quality bonds. The challenge is that those bonds, as of year-end 2022, were only worth $76 billion due to the rising interest rate environment of 2022, as disclosed in the firm’s 10K in late February 2023 and shown below:

When the firm had to sell bonds from its HTM portfolio, significant financial losses would be realized.

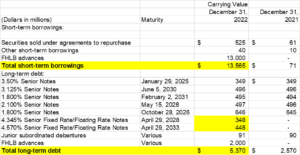

5. Invest Long and Borrow Short?

Perhaps the long-term bond holdings would not have proven so problematic if the balance sheet had long-term liabilities to match the long-term assets.

Looking at the balance sheet, we see from the table below that short-term borrowing was more than twice as much as long-term borrowing. We also see that the firm issued two notes during 2022, but the total of less than $800 million shown below was both fixed/floating, and the total was less than one-half of one percent of the balance sheet.

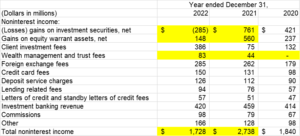

6. Losses from Investment Portfolio

The net loss shown above, of $285 million, rolls up into noninterest income. As shown below, management was trying to grow client investment fees and wealth management, but the sharp decline in the value of the investment portfolio which led to recognized losses in 2022 and less profit on equity warrants caused noninterest income to decline by almost $1 billion.

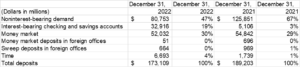

7. Nonsticky Short-Term Deposits

Just as the S&L’s of the late 1980s and early 1990s had long-term loans and fixed-income securities on the asset side of the balance sheet and short-term deposits and borrowings on the liability side of the balance sheet, which led them vulnerable to disintermediation and losses when interest rates rose, SVB also had long term loans and fixed income securities on the asset side and short-term borrowings on the liability side. Now let’s see if SVB had a short-term deposit structure as well:

Reliance on noninterest-bearing demand deposits was declining (likely as a result of clients in the start-up phase using cash balances in a challenging economic climate), and time deposits had increased, as shown above, but it was too little, too late. For readers who missed what an S&L deposit structure looked like in the 1980s, that’s okay; see the table above.

Looking Ahead

The bank failed when a run on the bank resulted in more than $42 billion of withdrawals in less than 72 hours. As management struggled to liquidate assets to honor the withdrawals (the bonds that had to be sold to meet that demand for cash had over $17 billion in losses to be recognized), underwater security sales resulted in further losses, which exacerbated the run.

The financial institution had long-term under-water assets and short-term liabilities and couldn’t meet cash demands. Regulations are likely to be proposed, and executives at financial institutions will be reviewing their balance sheet structure as well as what reporting requirements will likely be required by regulators.

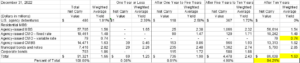

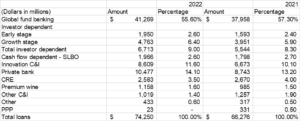

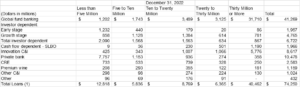

At Perficient, we see a few reports that will likely be required by regulators and, even if not, are valuable to management. One is that while loan concentrations are currently reported, deposit obligation concentrations are not. Consider the way SVB was reporting the concentration of their loans by the borrower type as shown below:

Now, consider how both management and regulators would have been better prepared, had the related deposits been reported the same way. Founders Fund instructed all the portfolio companies it had invested in to pull their mostly uninsured deposits from SVB. Several other venture capitalist firms did the same, and as a result of a handful of decisions, hundreds of firms withdrew tens of billions of dollars.

Nothing in the Call Report, FR Y-14, 10-K, 10-Q, or Y-9A reports mandates that the concentration of linked depositors to be reported. This may be of value to regulators and the management of financial institutions going forward. This could be an expansion of the 2052a liquidity report, the biggest arrow in the regulator’s liquidity reporting quiver. The SVB failure was ultimately due to a liquidity run. As reporting changes occur, Perficient will report them and work with clients to meet their changing regulatory reporting needs.

Model Risk

In addition, we at Perficient consider that model risk will once again become center stage. What happens if rates rise by x%? The vast majority of financial services firms, including SVB, passed their last CCAR (or DFAST for brokerage firms) report. However, just because a model says things will be fine doesn’t mean they will be. The assumptions and risks of models will likely be a focus in the next series of on-site bank examinations as well as CCAR/DFAST submissions.