In addition to the iPhone 6, iPhone 6 Plus and Apple Watch unveiled this afternoon, Apple also announced Apple Pay, the long-awaited mobile payments platform, creating quite a buzz in the payments and financial services industry. Apple has taken a leap of faith jumping head-first into contactless payments, biometrics, wearables and tokenization with the new iPhone 6 and Apple Watch. Many payment startups, mobile operators and even tech giants like Google, have failed to see widespread consumer adoption of mobile payments platforms for a number of reasons: a lack of added value, a poor user experience, data security and privacy concerns, retailer resistance and countless other barriers. I think this move will solidify not only their ability to disrupt payments, but is only the beginning of their master plan to revolutionize consumers’ financial lives and shake up the financial services industry.

What will make Apple Pay successful and why does it matters to financial services companies?

Apple’s Leadership Position and Stakeholder Buy-in

Apple is known for its ability to not only disrupt but also be recognized for its leadership position in the industry pushing the boundaries of technology innovation as they’ve done in the past with the iTunes Store, iPad and MacBook products. Few can rival the success Apple has consistently had and will continue to have as the company expands its business beyond the traditional smartphone and tablet market into new areas. This is can be a very important “win” for banks and financial services companies looking for ways to help make consumers’ financial lives better.

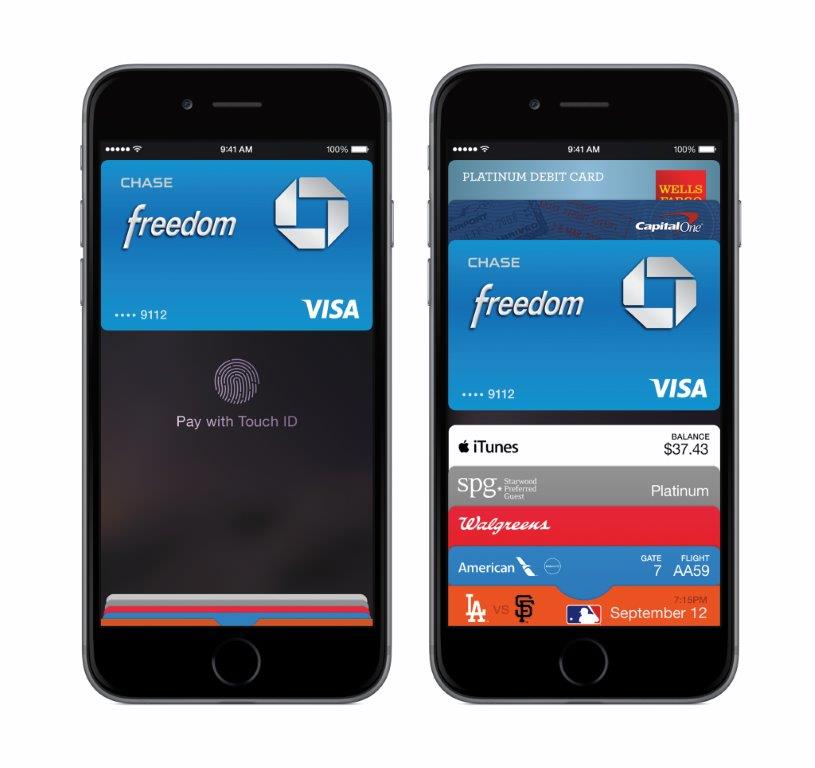

To gain consumer adoption of mobile payments, it takes a lot of promotion, education and collaboration on the parts of the banks, retailers, and technology developers. Already we’re seeing a partnership with and collaboration from the three major payment networks: MasterCard, Visa and American Express. Debit and credit cards issued from banks like Capital One, Bank of America, Chase, Citi and Wells Fargo, will be an important component to bring Apple Pay’s seamless mobile payment experience to their customers. These banks account for 83 percent of credit card purchase volumes in the US. According to Apple’s press release, some of the nation’s leading retailers will support Apple Pay, and Apple Watch will also work at over 220,000 merchant locations across the US that have contactless payment enabled.

Facing Vulnerability and Privacy Concerns

Data security and privacy are often viewed as top concerns for mobile banking and mobile payment applications. The almost daily news of data breaches has tarnished consumers’ trust in the credit card industry and the recent iCloud hack leaves Apple with something to prove. The Touch ID, Find My iPhone, and Secure Element features may very well be the missing links to improve consumer sentiment toward mobile payments and finally ditch their credit cards and physical wallets. Apple Pay is a also step in the right direction for card issuers abandoning magnetic stripe cards and aligns well with EMV adoption that will require retailers to upgrade point-of-sale systems with NFC readers. NFC stores encrypted ‘Device Account Numbers’ tied to an iTunes account, and the use of tokenization technology adds another level of security to the transaction building consumer trust. Another interesting bit of news, Apple won’t collect or save transaction information, purchase history or sell credit card data like other merchants and other third-party providers. This is a good move by Apple to build loyalty and trust with customers.

The Apple Experience

In perfect fashion, the Apple announcement comes on the heels of eBay’s “One Touch PayPal” service. Although they may face some stiff competition with PayPal’s penetration of the Android platform, Apple is known for their simplistic mobile design that instills a more seamless user experience on their devices. Finally Apple is extending their use of Passbook to serve as storage for debit and credit cards from an iTunes account. This “digital wallet” feature allows users to easily switch between cards to complete and view recent transactions.

Digital transformation in financial services begins with understanding customer behaviors, preferences and choices. Financial institutions are seeking ways to integrate their mobile and digital services as part of consumers’ daily lives. Apple’s products do just that. In one natural motion the iTouch ID fingerprint reader simplifies the transaction and payment experience for consumers. Banks need more control over the customer relationship and freedom to compete in order to change consumer behaviors. Apple is positioned better than any other company to help mobile banking and payments reach critical mass.

Integration and Partner Network

The potential for Apple Pay to be integrated with apps like Uber, Target, Groupon, Open Table, and Starbucks for in-app payments opens the door to endless possibilities not only in retail but in financial services. Similar to the business model and goal to extend the “Uber experience” with a growing partner network, Apple will leverage an API in iOS 8 to allow other app developers to integrate Apple Pay into their e-commerce applications.

Although some financial institutions have piloted or launched payment innovations, a vast majority have held off on investments in fear that consumers may still be wary of mobile wallets. Apple’s product announcement opens up new doors for banks to leverage their mobile payments platform and SDK to facilitate the development of customer-facing mobile apps. NFC promises to enable new mobile features for loyalty and rewards, payments, couponing and marketing to deepen customer relationship – something that banks are all seeking to accomplish with mobile. I think we’ll see a strong movement from banks and financial services companies jumping on the Apple bandwagon. Playing within the traditional payment rails and growing Apple user community is to a bank’s advantage. I expect to see increased investments in mobile and payments innovation to encourage mobile banking adoption and uncover new revenue sources or channels for engagement.

Apple has the potential to be the future “hub” for financial technology innovation and payments integration on a global scale. I think this area is one of the things I am most excited about with the new iPhone 6, Apple Pay and Apple Watch. This by far surpasses any speculations others may have had with Google disrupting financial services or questioning if one day there may be a “Google Bank”. Apple’s ability to deliver one-touch payments and mobile apps that can add value to my everyday financial and commerce activities as a consumer is remarkable. In this case, the “last mover advantage” I think will pay off for Apple and financial institutions waiting to see where the market was headed with mobile payments.

Will Apple’s announcement change your institution’s mobile strategy and approach to financial services innovation?